It’s the game of generating income grow and private equity firms remain in it for the long haul (or a minimum of until they reach their rate of return, then they’re gonna offer).

Their performance matters both for investors and the broader economy MOST APPARENTLY noise stewards of capital were revealed to be anything but throughout the 2007-09 financial crisis. Bank bosses were shown to have taken on too much risk. Star hedge-fund managers suffered losses. Nor have the years ever since been kind. athletes sports agencies.

The private-equity (PE) industry has been an exception to the trend. The funds it released during the crisis in 2007-09 have ended up yielding a typical annualised return of 18%. And it has ended up being far more essential. Investors, from university endowments to public pension funds, have actually handed over ever more money to PE supervisors (see chart).

Assets under management have swollen to more than $4trn. The 8,000 firms run by PE in America represent 5% of its GDP, and a comparable share of its workforce. Now another savage economic downturn is in full swing and the efficiency of PE is a vital question for investors and the economy.

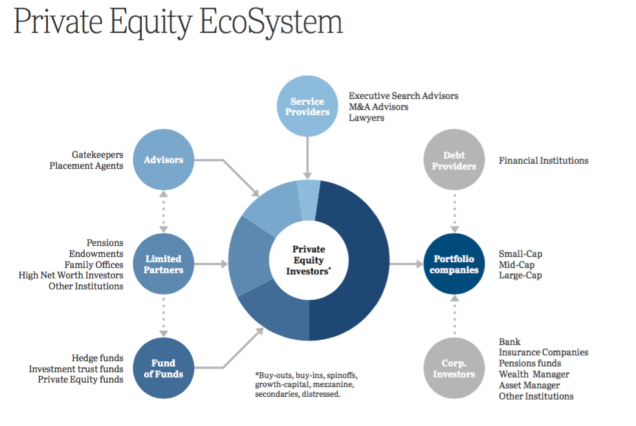

Specific funds can have their own timelines, investment objectives, and management philosophies that separate them from other funds held within the very same, overarching management firm. Effective private equity companies will raise many funds over their lifetime, and as firms grow in size and intricacy, their funds can grow in frequency, scale and even uniqueness. To get more info regarding private equity and also - research his blogs and -.

In 15 years of handling possessions and backing numerous entrepreneurs and financiers,Tyler Tysdal’s business managed or co-managed , non-discretionary, approximately $1.7 billion in assets for ultra-wealthy households in markets such as healthcare, oil and gas , real estate, sports and entertainment, specialized lending, spirits, innovation, consumer goods, water, and services companies. His team recommended clients to purchase almost 100 entrepreneurial companies, funds, private financing offers, and real estate. Ty’s track record with the private equity capital he deployed under the very first billionaire customer was over 100% yearly returns. Which was during the Great Recession of 2008-2010 which was long after the Carter administration. He has developed hundreds of millions in wealth for clients. Provided his lessons from working with a handful of the certified, highly sophisticated individuals who might not seem to be pleased on the advantage or understand the possible drawback of a offer, he is back to work entirely with entrepreneurs to help them sell their companies.

Meanwhile they have actually accumulated $1.6 trn in dry powder that they can deploy on new deals. PE shops’ fate depends upon whether the hit to their existing financial investments is nasty enough to erase the prospective gains from dealmaking paid for by the crisis. Start with the potential losses. In the first quarter of 2020 the 4 big noted PE companies, Apollo, Blackstone, Carlyle and KKR, reported paper losses on their portfolios of $90bn.

After an early scare PE firms’ shareholders have actually concluded that the outlook is relatively bright (see chart). Are they right? Numerous PE supervisors have been energizing returns by piling debt on to the business they buy. In the years right away after the last crisis most buy-out deals were finished with debt worth no greater than six times gross operating profits.

That would suggest that PE-run firms are susceptible. More than half of the 18 junk-rated firms that defaulted in the very first quarter of the year were PE-owned, according to Moody’s, a ranking company. It anticipates the total junk default rate to triple to 14% by 2021 (private equity firm). Over the previous years PE financing has shifted far from dopey, sidetracked banks towards expert private-credit firms.

3 Misconceptions Of Selling To Private Equity Firms + Lutz M&a

And making things harder still, most big PE managers say that the companies they own are either ineligible for, or unwilling to tap, the American federal government’s service bail-out plans, the Paycheck Security Program and the Main Street Financing Programme. Even so, several other aspects might have changed to work in PE’s favour.

Considering that the 2007-09 crisis many PE supervisors have actually likewise set up substantial credit armsfor the huge 4 firms, these now account for a third of their assets. They might give managers more in-house competence and systems for raising financial obligation, making it much easier to reorganize the debts of fragile portfolio business on favourable terms.

” There is a bothersome gap,” states Marc Lipschultz, co-founder of Owl Rock, a private-credit fund. “We do not understand how deep or how wide it is, however funds require to find a bridge across. harvard business school.” And if PE-run companies can not raise more debt, default or reorganize their loanings, the staying option is an “equity treatment”: PE stores stump up the cash to keep their firms afloat.

The way funds are structured ways that supervisors can not release their “dry powder” raised for brand-new funds into companies owned by older ones. local investment fund. But most older funds do have huge reserves. Michael Chae, the primary financial officer of Blackstone, states that around $30bn of its $152bn of dry powder is set aside for them.

Usually, a PE fund returns cash to its investors when it offers its stake in a companybut if the financial investment period is still continuous, the fund can ask for it back. According to an industry body for PE investors, the number of calls for such “recycled capital” has actually risen. Bailing out existing investments will drag down returns for PE shops.

A lot of PE managers hope to use their newly expanded credit arms to scoop up bombed-out loans and bonds with collapsed pricesLeon Black, the founder of Apollo, has stated the chance is “massive”. But the volume of standard buy-outs dropped sharply in March, and just a few firms have because made purchases.

Now it is time to strike. Editor’s note: A few of our covid-19 protection is complimentary for readers of The Economist Today, our everyday newsletter. For more stories and our pandemic tracker, see our coronavirus centerThis article appeared in the Finance & economics section of the print edition under the headline “More money, more problems”.

What Happens When Private-equity Firms Start Making Deals

As Warren Buffett said, “Guideline primary: Never lose cash. Rule number 2: Always remember guideline top.” Whether you are the CEO/founder of a start-up or an older, privately held organisation, there may come a time where you and your associates are seeking outdoors capital. In an ideal world, you are doing so to grow and scale a service due to demand.

Whatever the case may be, your campaign to raise outdoors capital will certainly involve sophisticated investors like private equity investors deeply inspecting your current finances and prospective to provide an appealing return (securities exchange commissio). Essentially, if you are thinking about outside capital from private equity investors, you need to ask yourself one crucial concern: “Is my company all set for the demands of private equity?” As the president of a nationwide executive search firm, I frequently encounter scenarios where private equity firms are exerting significant pressure on their portfolio business to adhere to higher performance standards.

Much of these circumstances require us to replace the existing CFO with a private equity skilled candidate. So why do private equity firms do this? As mentioned by Buffett, it is to safeguard their financial investment. Specifically if the private equity firm is investing eight or nine figures into your business, the stakes are very high.

Particularly, I will talk about some substantial modifications in terms of reporting standards and personnel that private equity companies require of portfolio business. Despite the financing source, companies that obtain outside capital are having fun with raised stakes. Lax compliance standards or incomplete monetary statements are simply out of the concern.

Often, portfolio companies offer this clarity through more detailed financial declarations – securities fraud theft. In reality, this increased level of detail might be a mandatory part of the fundraising round. As just one example, many private equity companies require their portfolio companies to have a hard close each month. Numerous private business bypass this practice each month, rather choosing to do it every quarter or every year.

If the portfolio business does not have the resources to rapidly implement a regular monthly close, it may develop some considerable obstacles within the organization. In addition to a regular monthly hard close, private equity firms typically set up rigid monetary preparation and analysis (FP&A) requirements. These FP&A requirements may include things like capital forecasts, EBITDA (incomes before interest, tax, devaluation and amortization) bridges and more.